Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

The #1 Thing Sellers Need To Know About Their Asking Price

When you decide to sell your home, your goal is simple: get it sold quickly and for the best price possible. Totally fair, right? But here’s the thing—too many sellers today are aiming way too high, without realizing the market has shifted. Inventory has grown, and we’re not in the same wild seller’s market we saw a couple of years ago.

The result? More price cuts. And not the fun “clearance sale” kind.

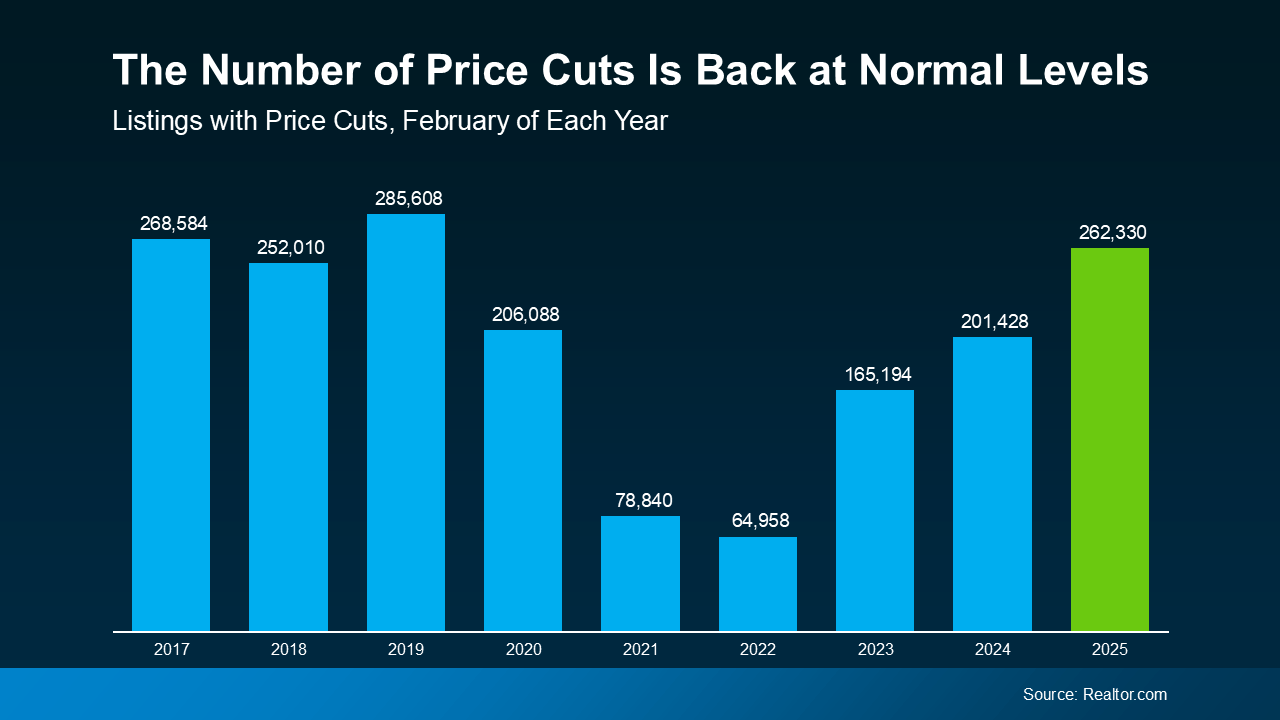

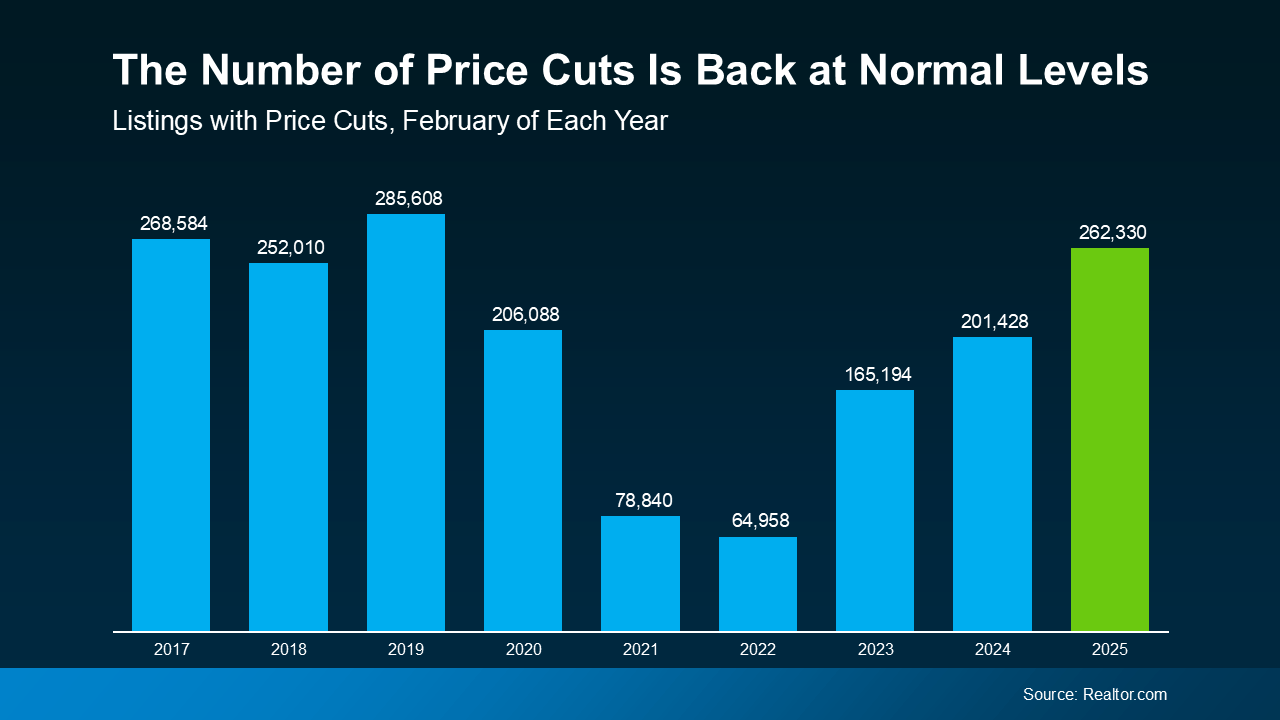

According to Realtor.com, February saw the highest number of price cuts for that month since 2019.

That’s right—more than any other February in the last six years.

If you consider that 2019 was the last true normal year for the housing market – that’s a big deal. We’re getting back to what’s typical for the market.

Why does that matter? Because 2019 was the last “normal” market before all the pandemic-fueled chaos. We’re now getting back to that more balanced environment, and that means it’s time for a mindset shift—especially when it comes to pricing.

Expectations vs. Reality

You might not get the same number your neighbor got during the height of the frenzy. And if you overshoot and then have to lower your price later, you could end up walking away with less than if you had just priced it right from the beginning. Ouch.

So how do you get it right? Simple: lean on your agent (hi 👋🏼).

How I Help You Price It Right

I don’t just throw a number out there and hope it sticks. I use real-time data, local trends, and my own nerdy obsession with market stats to land on a number that makes sense for your home.

Here’s how we make that magic happen:

-

Recent sales: We look at what homes like yours have actually sold for—not what they were listed at, but the final closing number.

-

Local market trends: It’s not just about what you want for your home, it’s about what buyers are willing to pay in today’s market.

-

Strategy: Depending on demand, we might even price just below market value to create urgency and attract multiple offers.

Why Starting Too High Can Hurt You

Now, I get it. Some sellers want to “test the waters” with a higher number. Maybe you’re hoping a buyer will fall in love and pay full price or more. But here’s the truth: that strategy often backfires. Big time.

-

Buyers might not even look at it. If it seems overpriced, it’s skipped. Boom—off the list.

-

It could sit too long. A stale listing makes people wonder, “What’s wrong with it?”

-

You may end up with less. Homes with price cuts often sell for less than they would’ve if priced right from day one.

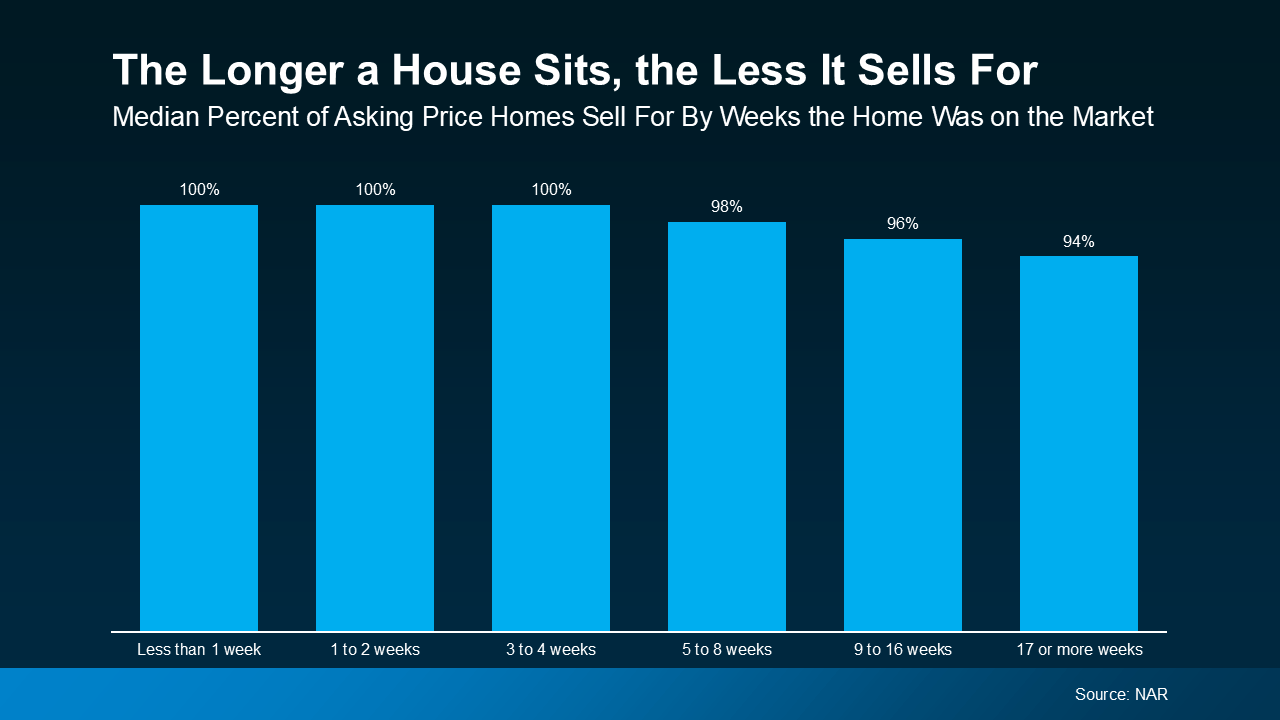

The National Association of Realtors even has data that backs this up. Homes that sell within the first four weeks usually go for full price. The ones that linger? They tend to sell for less. It’s like the housing version of “you snooze, you lose.”

Bottom Line

You don’t want to chase the market by listing too high and then playing catch-up. You want to get it right the first time.

So, let’s talk strategy. If you’re thinking of selling, I’m here to help you figure out a pricing game plan that brings in serious buyers, not just tire-kickers. No gimmicks, no fluff—just honest advice with a little dad-joke flair if you need it.

Want your home to sell fast and for a great price?

Let’s connect.